Invest

Investors Incorporate ESGs Into Long-Term Portfolios

In the last ten years, Environmental, Social and Governance (ESG) considerations have been incorporated into long-term institutional investors’ portfolios.

This has been done through the creation of ESG mandates or by incorporating ESG criteria across the entire portfolio.

Adding ESG criteria into long-term portfolios raises some important questions:

• What is the impact of ESG on portfolio performance and characteristics?

• How does it alter the risk profile and the factor exposures of portfolios?

• How does it affect investors’ ability to pursue their investment strategy?

To answer these questions, we first analysed the relationship between ESG characteristics and traditional risk factors. We found that ESG scores had positive correlations with size, quality and low volatility. Then we assessed the impact of ESG integration on different investment strategies through a consistent portfolio construction framework. Our results show that integrating ESG criteria into passive strategies generally improved risk-adjusted performance over the period 2007 to 2016 and tilted the portfolio toward higher quality and lower-volatility securities.

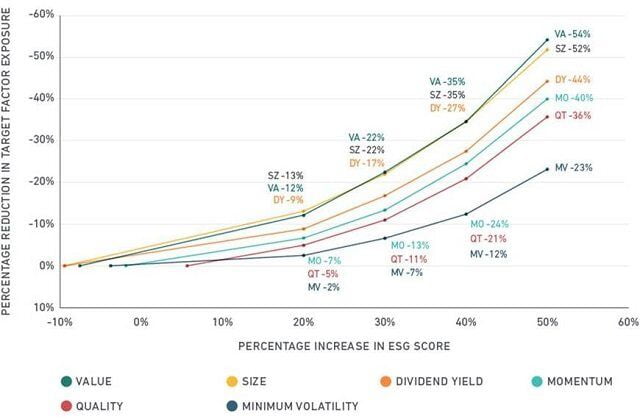

When we integrated ESG into factor strategies, we found that significant improvements in the ESG profile of these strategies was achieved with relatively modest impacts on target factor exposure, as seen in the exhibit below. However, not all strategies were affected to the same extent. In particular, minimum volatility strategies experienced only a 7% reduction in target factor exposure for a 30% enhancement in their ESG rating. On the other hand, value strategies incurred a 22% reduction in target factor exposure for a similar 30% improvement in their ESG characteristics. When we seek to achieve more substantial ESG improvement, the reduction in target factor exposure becomes greater. For 50% ESG enhancement, the impact on target factor exposure ranged from 23% to 54%.

The Effect of ESG Scores On Target Factor Exposure

Our results suggest that passive investors would have been able to improve the ESG characteristics of their strategies without a negative impact on their ability to capture market returns efficiently. Defensively oriented factor strategies (where ESG had positive correlation with the target factors), such as high quality and low volatility, would have benefited from incorporating ESG. Even dynamic strategies, such as those based on the value and momentum factors, could have enhanced their ESG profile with only a modest impact on target factor exposures and ex-ante information ratios.

These results may provide guidance to passive and active managers who wish to incorporate ESG criteria into their strategies. They show that historically ESG has generally improved the information ratio of many typical passive and factor-based investment strategies. They also show that the impact of ESG on ex-ante information ratios of these strategies is relatively moderate and varies according to the primary investment objective and target factors of the underlying strategy.

Finding the Best Eco-Friendly Crypto Listing Agencies

Do Eco-Friendly Homes Sell Faster or Just Look Better?

A Breath of Fresh Air: Your Guide to Eco-Friendly Roofs

Eco-Friendly Home Upgrades That Start With Sustainable Tiles

Cool Your Home Naturally: Green Alternatives to Cranking the AC

Cutting Contamination Off At The Tap: Fighting PFAS At The Source

The Hidden Environmental Cost Of Your Grocery List

The Future of eBike Tech: What to Expect in the Next 5 Years

Eco-Friendly Sustainable Building Materials to Consider

Sustainable Driveway Upgrades for Everyday Homeowners

Cool Your Home Naturally: Green Alternatives to Cranking the AC

The Hidden Environmental Cost Of Your Grocery List

Cutting Contamination Off At The Tap: Fighting PFAS At The Source

The Future of eBike Tech: What to Expect in the Next 5 Years

Eco-Friendly Home Upgrades That Start With Sustainable Tiles

Do Eco-Friendly Homes Sell Faster or Just Look Better?

A Breath of Fresh Air: Your Guide to Eco-Friendly Roofs